Building a Portfolio

5 Pillars of Portfolio Construction

Building a portfolio is not a random collection of good ideas. It is a disciplined engineering process. I view portfolio construction through five critical lenses that balance return objectives with structural constraints.

Popular Asset Classes

Market Indexes

A market index is a number that tracks the performance of a specific group of securities. For example, the S&P 500 tracks the 500 largest companies in the U.S., while the TSX Composite tracks the headline Canadian market. Investors "buy" an index through an Exchange-Traded Fund (ETF).

Markets are generally efficient over the long term. By using ETFs that track broad indices, you can achieve instant diversification across sectors (Financials, Energy, Tech) at a fraction of the cost of active management.

Some popular ETFs in Canada include

- VFV (Vanguard S&P 500 Index ETF): The most popular way for Canadians to own companies in the S&P 500. It is "unhedged," meaning you also gain exposure to the USD/CAD exchange rate.

- VDY (Vanguard FTSE Canadian High Dividend Yield): Heavily weighted toward the "Big Five" banks and major energy infrastructure (utilities/pipelines).

- XIU (iShares S&P/TSX 60 Index ETF): This ETF tracks the 60 largest, most established companies on the TSX.

- XEQT (iShares Core Equity ETF Portfolio): 100% Equity. Highly popular for its ultra-low MER (approx. 0.20%) and exposure to over 9,000 global stocks.

Fixed Income

Fixed income refers to investments where the borrower (a government or corporation) is obligated to make payments of a fixed amount on a fixed schedule. This includes Bonds, GICs, and Treasury Bills (T-Bills).

Fixed income is a tool for Volatility Management and capital preservation, in other words it is typically viewed "safer" than equities. Bonds provide a predictable cash flow (coupons) and typically have a low-to-negative correlation with equities during market stress.

Individual Equities

Equity represents an ownership stake in a corporation. When you buy a share of a company, you are entitled to a portion of its assets and earnings, what we think of when we say "stocks". Unlike fixed income, there is no guaranteed payment; the return comes from Dividends and Capital Appreciation.

Historically, equities have outperformed all other major asset classes over long horizons. However, equities sit at the bottom of the capital structure. In a liquidation, shareholders are paid last. This makes the stock price highly sensitive to market sentiment, interest rates, and earnings misses. Regulatory changes, management scandals, or technological disruption (e.g., the "AI threat" to legacy software) can destroy a single company’s value even if the broader market is rising.

Other Asset Classes

My Personal Portfolio

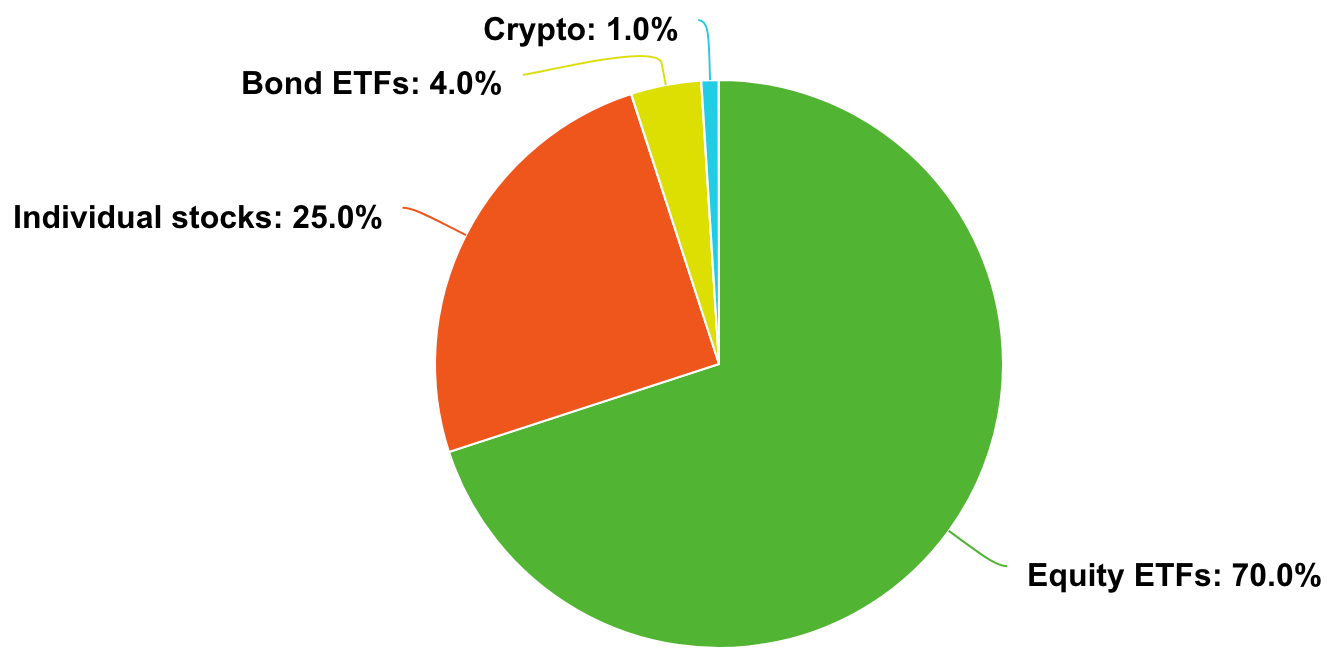

My investment mandate follows a Core-Satellite model. The "Core" of the portfolio consists of 70% North American Equity ETFs, providing low-cost, diversified exposure to the Canadian and US economies. This is stabilized by a 4% allocation to Bond ETFs, acting as a volatility buffer.

Surrounding this core is the "Satellite" component, 25% in Individual equities and a 1% allocation to crypto. I apply fundamental bottom-up analysis to identify undervalued securities and emerging technologies that have the potential to outperform the market